Last Updated: 13-01-2021

Reading Time: 4 minutes

Earlier in September, we saw six of the biggest lenders withdraw 10% deposit mortgages. This unprecedented move has decimated the first-time-buyer market in one fell swoop.

What’s behind the move? Why have so many banks looked at the market and decided there’s a new level of risk attached to buying houses? Let’s take a look.

Bottlenecks, Backlogs and Build-up

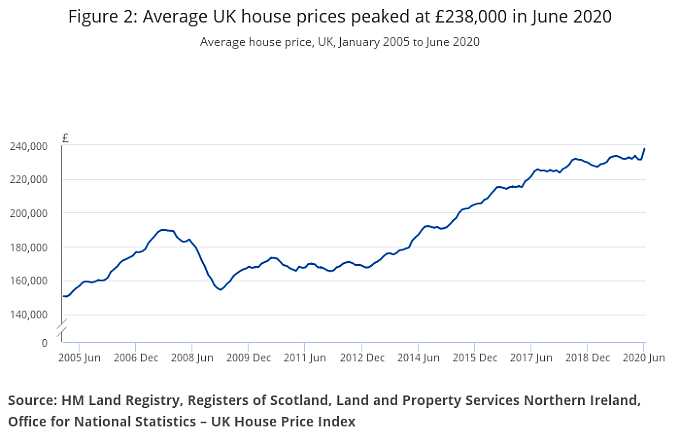

During the UK’s lockdown period, house sales stopped. Estate agents, valuers, prospective buyers: no one was coming to look at your house.

This inactivity, quite naturally, caused a bottleneck. So, when the housing market reopened in June, it was busy. Even up to time of writing, house prices in some regions are rising. Sales are still relatively strong.

But market experts predict that this flow is not sustainable. Once the surge has been satisfied, the market will dip once more. Here are the reasons experts are predicting as much.

The False High

House prices have defied market predictions by not only holding up their end, but even rising. Experts tell us that pent-up demand is pushing up those prices. Vendors know buyers are desperate to move and are sticking to their guns with their sale prices.

This is creating a false high. Once the backlog is satisfied, prices will flat-line.

Lenders are aware that prices may drop by several percentage points in a short space of time. The bigger the deposit a buyer puts down, the less chance the home will fall into negative equity.

But there are other drivers behind the current house price and minimum deposit hikes.

Lifestyle Choices

In London, we’re already seeing prices drop. City dwellers experienced the downside of living in a concrete jungle during lockdown. Should lockdowns become regular, they’ve decided they don’t want to subsist in small apartments.

Convenient for the commute they may well be. But when you’re in lockdown, confined to barracks? One can only imagine the claustrophobic atmosphere such apartments imbue.

Today, what was only a whisper of people moving to the suburbs has become a movement. People want space, gardens, multiple rooms (including room for a separate home office).

This need will push up prices in properties in the green belt and suburbia as the dust settles.

But the amount of housing on the outskirts of cities is finite. It doesn’t help that the government’s behind on new housing schedule commitments. All things considered, any exodus from the city could soon fall into a forced hiatus.

Buyers (and vendors) know this, and so should you if you’re planning to move. If you’re desperate to move, you may have to take a short-term loss on the chin. The value of your home may drop before prices stabilise.

Recession and Unemployment

All but guaranteed is the prospect of widespread job losses at furlough end in October. Many thousands of workers have already seen their jobs bite the dust.

Upon the market reopening, we’ve seen a change in tack from underwriters. Before COVID-19, the big question they asked of contractors was how much can you afford?

This question now has a critical partner in crime: in which industry do you work?

Lenders want to know whether you’ve been on furlough. They want to know if you’ve taken a payment holiday. They want to know what industry you work in. More accurately, is that industry susceptible to another wave of COVID-19 and lockdown?

This new risk is a very real new level of lending criteria that lenders are imposing. Many lenders have already stated that they’ll not lend to furloughed workers.

And it’s not only applicable to contractors and the self-employed. Lockdown susceptibility is relative to all homeowners, no matter how they work/get paid.

Negative Equity

With the recession, lenders are expecting house prices to eventually drop away. They’re expecting people to be made redundant. They’re expecting people to not be able to keep up their mortgage repayments.

This is the crux of the withdrawal of 10%-15% deposit mortgages. Should banks have to repossess your home, they do not want to lose out on the deal.

If you have put 20% down, the chances are the property will retain at least 80% of its current value. That’s what lenders are banking on, at least.

Are lenders really expecting a 10%+ drop in house prices?

I don’t think house prices will drop so sharply. What I do think is that lenders are aware of the backlash of the financial crisis in 2007/8. The higher deposits are a safety net to ensure they’re neither exposed nor blamed again.

You will have noticed that interest rates are also rising, seemingly unchecked. Moneyfacts reports the “steepest rise in fixed rates for a decade.” Again, this is a pre-emptive move by lenders to ‘future-proof’ themselves.

Is the withdrawal of 10% mortgages too much of a knee jerk reaction, then?

Maybe these measures seem harsh, but lenders have taken them with sound intentions. They are aiming to provide the ‘Responsible’ lending that the FCA demands of them.

But there is another Dementor creeping back into the headlines again: Brexit. It adds another level of the great unknown we’re all facing right now.

I hope that lenders are practising that old adage: hope for the best, prepare for the worst. Because, despite the challenges we’re already facing, the worst may yet be to come.

What should I do if I want to sell and/or move home?

It’s not all bad news, though. Under current temporary measures, homebuyers pay 0% SDLT on homes <£500,000. There are calls for the government to extend this Stamp Duty “holiday”.

The increased threshold has helped the current wave of buyers in today’s market. And with the background outlined above, it will need a prop of some sort to maintain their interest.

For any contractor, freelancer or director wanting to buy or sell today, don’t go in blind. Speak to an authority on mortgages, one who understands how you work.

A specialist broker can match your scenario with the most appropriate mortgage and lender. Moreover, they’ll be able to prove your affordability to cautious lenders and underwriters. That will be key to your success as lending criteria tighten along the road ahead.

John Yerou is a pioneer of contractor mortgages and owner and founder of Freelancer Financials, Contractor Mortgages®, C&F Mortgages and Self Employed Mortgages, trading styles and brands of the award-winning Mortgage Quest Ltd.

Twitter

Twitter Facebook

Facebook Linkedin

LinkedinPosted by John Yerou

on September 28th, 2020 14:40pm in John’s Blog.